Real-time data observability is the missing layer in EU AI Act compliance

How financial institutions can turn pipeline evidence into a competitive advantage

Most European financial institutions have taken the right first steps toward EU AI Act compliance. Governance committees are in place. Model risk frameworks have been updated. Responsible AI policies are signed off at the board level, and Article 10 sits inside the compliance workstream. On paper, the governance layer looks solid.

The problem surfaces the moment a regulator arrives and starts asking for evidence.

Picture a mid-sized European bank running a credit scoring model across three EU member states. The model documentation is thorough. The AI ethics policy has board sign-off. The model inventory is current. But when the ECB’s supervisory team asks whether the training data was representative of the applicant population at the point of training, and whether data quality was continuously monitored through the pipeline, the data engineering lead cannot answer.

What does not exist is an automated, timestamped audit trail proving that representativeness was measured, that quality gates ran at each pipeline stage, and that issues were documented and resolved before the data reached the training job. There is no evidence of execution, only evidence of intent. The governance framework describes what should have happened. The data pipeline is the only place that can prove it did.

Article 10 exists because the introduction of AI into high-stakes financial decisions created a new category of data risk. When a credit decision, an AML flag, or a fraud alert is generated by a model, the quality, representativeness, and fitness of the training data become a direct input to outcomes that affect individuals’ financial lives and institutions’ regulatory standing. As enforcement begins on August 2, 2026, the gap between governance policies and pipeline-level proof of adherence to those policies is where most financial institutions remain exposed.

What Article 10 actually requires

Regulation (EU) 2024/1689, Article 10 sets out five concrete, enforceable requirements on training datasets. For data and technology teams in financial services, understanding them in practical terms is the starting point.

- Training data must be demonstrably relevant and representative of the population the AI system operates on. This requirement is fundamentally about data scope: the data used to train the model must reflect the same population and operating conditions the model will encounter in production. That means measured and documented analysis, not a conceptual assertion in a policy document.

- Processes must be in place to detect, measure, and remediate data quality issues, and those processes must be provably operational. This is the data quality and observability requirement. A clean dataset with no quality-monitoring history is harder to defend than one with documented issues and remediation, because the absence of monitoring records is itself a compliance gap.

- Data must have appropriate statistical properties. Distribution analysis, completeness metrics, and feature-level profiling are the practical tools here. Skewed distributions, missing values concentrated in specific subpopulations, or feature correlations that encode protected characteristics all fall within scope.

- Datasets must be examined for possible biases that could affect health, safety, or fundamental rights before a model is trained. This obligation must be met at the data level, before training begins, and is separate from model fairness testing, even though both are required.

- A documented, auditable record is required that covers where the training data came from, what transformations were applied, and what its quality looked like at each pipeline stage.

The common thread across all five requirements is evidence of adherence. Having an internal policy that reflects the expectations of Article 10 in the institution’s own language is the necessary first step. What regulators are asking for is proof that the policy was actually followed: automated, timestamped records demonstrating that the controls described in the policy were operational for a specific dataset at a specific point in time.

Why financial services face heightened scrutiny

Annex III of the EU AI Act explicitly classifies creditworthiness assessment, credit scoring, insurance risk assessment, and underwriting as high-risk AI systems. The supervisory infrastructure to enforce compliance is already in place. The EBA’s November 2025 guidance on AI Act implications for the banking sector identified the quality and representativeness of training data as an ongoing supervisory priority, clearly signaling where examiners’ attention will focus when enforcement begins.

Article 10 does not replace existing model risk management obligations under the EBA Guidelines on loan origination and monitoring. It extends them into territory most MRM processes have not yet reached: the quality, observability, and fitness of training data specifically. Institutions that believe their existing governance and model risk frameworks are sufficient have likely addressed the intent of Article 10, but not yet the evidentiary obligation it creates.

The real gap is in the pipeline, not the policy

A policy stating that training data must be representative creates an obligation. It does not fulfill one. The moment a regulator asks for evidence that representativeness was assessed, measured, and documented for a specific dataset at a specific point in time, the policy becomes irrelevant. What matters is whether the data pipeline generated that evidence automatically, or whether the team has to reconstruct it under audit pressure.

Financial institutions typically draw training data from dozens of source systems. By the time data reaches a model training job, it has passed through ETL and ELT processes, feature stores, and data lakes. At each stage, the lineage relationship between source records and the training dataset becomes harder to trace unless it was captured automatically. Most data quality programs compound the problem by focusing on detection after consumption: issues surface through downstream failures, after the data has already been used.

The result is that many institutions have policies in place but lack the infrastructure to prove compliance when it counts.

What a prevention-first approach looks like in practice

The institutions best positioned under Article 10 are those that have treated the regulation as a prompt to build the data infrastructure that should have existed anyway: data quality validation and observability engineered into the development processes themselves, embedded directly in the pipeline, generating continuous evidence of data fitness as a natural byproduct of normal operations.

The distinction matters. Observability alone tells you that data moved through a pipeline. Data quality validation tells you whether the data that moved was fit for the specific decision it informed, whether that is a credit scoring run, an AML screening process, or a fraud detection model. Embedding both together in the pipeline means every execution produces a timestamped, auditable record without anyone having to assemble it after the fact.

These requirements are not new to financial services. BCBS 239 established similar expectations for data quality and lineage in risk reporting. What has changed is the operating environment. The speed and scale at which AI models consume data, generate decisions, and create regulatory exposure have made the manual triage and reactive monitoring that once kept institutions compliant genuinely unworkable. Real-time observability is the layer that closes that gap: it gives data and risk teams the continuous visibility to catch issues as they arise in the pipeline rather than after a model has already acted on compromised data.

Continuous lineage completes the picture by tracing every training dataset record back to its source and documenting every transformation along the way. Automated profiling and distribution monitoring address the bias examination requirement upstream, surfacing representativeness issues before they reach the training job rather than after a model has been deployed.

For institutions already operating under BCBS 239 and DORA, this kind of auditable evidence trail is a familiar concept. Article 10 extends it into AI training data. When quality validation, observability, and lineage tracking are engineered into the pipeline, every execution produces a timestamped record automatically. When a regulator, auditor, or internal risk team asks for evidence, institutions retrieve it rather than rebuild it.

How Ataccama addresses Article 10 requirements

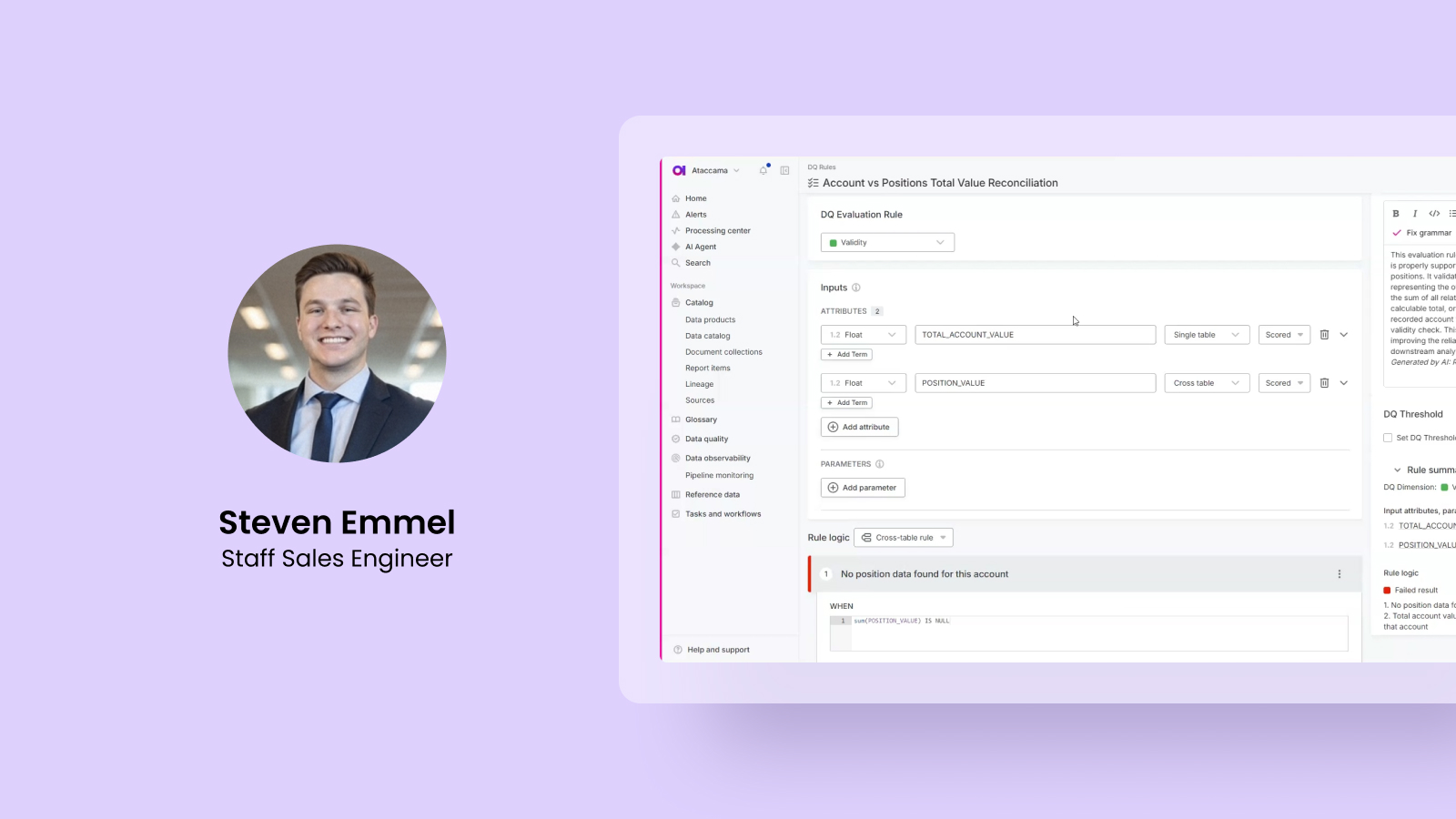

Ataccama ONE embeds data quality validation and observability directly into the pipelines that financial institutions rely on for credit scoring, AML monitoring, and fraud detection. The platform validates data against business-defined rules, checking completeness of borrower attributes, validity of transaction records, and consistency of risk signals before data is used downstream. Each validation is logged with pipeline context, creating a traceable record of whether data met defined standards at the moment it was used in a decision.

New capabilities announced in April 2026 extend this further. Pipeline Monitoring tracks data in motion across dbt, Airflow, Dagster, and AWS Glue in real time, capturing execution health, schema changes, and volume anomalies. Regulatory Impact Alerting consolidates pipeline and data quality signals into a single alert layer that prioritizes issues by regulatory and business impact, routing them to the responsible data owner with full lineage context. Audit-Ready Incident Traceability converts pipeline incidents into tracked records within Jira and ServiceNow, linking each issue to affected datasets, pipeline steps, and downstream AI processes, and documenting how issues were identified and resolved.

The result is that teams can produce on-demand evidence that specific data met defined quality standards at the time it was used, without manually reconstructing pipeline history after the fact.

To learn more about how Ataccama helps financial institutions satisfy Article 10 requirements for credit scoring, AML screening, and fraud detection, visit ataccama.com or download the EU AI Act Article 10 Readiness Checklist, which covers data lineage and traceability, representativeness and bias assessment, real-time quality monitoring, evidence trail documentation, and cross-environment consistency, mapped directly to Article 10’s requirements.

The path to compliance runs through data engineering

Policies, governance committees, and model inventories are the foundation. They establish the standards institutions are committing to meet and give regulators a framework to audit against. What they cannot do on their own is generate the operational evidence that Article 10 demands: the timestamped, automated proof that those standards were actually applied, in a specific pipeline, on a specific dataset, at a specific point in time.

Enforcement begins August 2, 2026. The institutions that will be ready are those that have closed the gap between governance intent and pipeline execution, making data quality and real-time observability part of their engineering infrastructure so that compliance evidence is generated as a matter of course, not assembled under audit pressure.

For a deeper conversation about what prevention-first data quality and observability looks like in practice for financial services AI pipelines, Ataccama’s team works with institutions navigating exactly these challenges. Get in touch: https://www.ataccama.com/contact.

Lauren Ruth

Lauren is the Director of Global Communications at Ataccama. With over a decade in the data industry, she specializes in strategic communications and has helped fast-growth startups define and amplify their data stories. She previously led communications at Alation and Informa Markets and holds a dual B.S. in Business and Communication, with a specialization in Technology, from Cornell University.