How data maturity impacts allocation: The competitive edge in asset management

Key takeaways

Problem: Investment decisions, speed to execution, and the ability to pivot post-investment are impacted when deal teams lack conviction in the underlying analysis.

Root Cause: Investors rely on data from company financials, analyst reports, market research, and third party vendors, tied together by late night reconciliation and validation done by the most junior members of the team. .

Solution: Establishing a data trust layer—combining data quality monitoring, observability, and cataloging—ensures that critical investment data is accurate, visible, and decision-ready across the deal lifecycle.

In a market where access to capital is abundant and deal flow is increasingly commoditized, differentiated returns come from speed and specialization. At many funds, however, the velocity of deal execution is bottlenecked by a hidden operational drag: data wrangling.

Investment firms are fixated on optimizing performance. They model sensitivity tables down to the second decimal place. But the governing assumptions behind all of that quickly fall apart if the data underpinning them is suspect. Gaining confidence in that data comes at a cost.

The data wrangling tax

Global private markets AUM reached approximately $13.1 trillion in 2023, according to the McKinsey Global Private Markets Review 2024. The capital has scaled. The data infrastructure supporting those assets largely hasn’t.

Public equities benefit from decades of standardization: CUSIP, ISIN, ticker symbols, and exchange-mandated reporting create a baseline of interoperability that asset managers simply don’t have. Private market data is inherently unstructured.

Asset management professionals spend a significant share of their time on data collection and management tasks rather than analysis and decision-making. The burden is especially visible in private markets, where data is inherently less standardized and often arrives in inconsistent formats. This mirrors broader findings in data-heavy roles, where up to 80% of time can be spent collecting, cleaning, and organizing data rather than generating insights. At a firm with ten investment professionals and an average fully-loaded cost of $300,000 per year, even a conservative estimate of 20–30% translates to roughly $600,000–$900,000 annually spent on work that produces no analytical output.

The workflow will be familiar to anyone who has worked in the asset class. Company financials arrive as PDFs or Excel files with inconsistent formats., Third-party market data from Bloomberg, CapIQ, or FactSet arrives in its own schema, requiring manual mapping before it can be compared against internal benchmarks. Historical deal data lives across systems, including the institutional memory of whoever ran the last investment process.

At most companies, none of this is handled by a dedicated data team. In middle market and growth equity, investment professionals are the data team.

The highest cost is the opportunity of what those hours could have produced: more deals screened, portfolio company conversations, or time on the specific analytical work that actually generates differentiated returns.

How data maturity impacts the deal lifecycle

Deal sourcing and screening speed

Companies with mature data practices make informed decisions on more deals faster. The reason for this is structural; when pipeline data is already normalized and enrichable, analysts can query a unified dataset rather than spending two days assembling the spreadsheet that makes the query possible in the first place.

Speed matters disproportionately in competitive processes. A company that can complete preliminary due diligence in eight days rather than three weeks has a structural advantage that compounds across a fund’s life. It sees more deals, makes faster passes on the ones that don’t fit, and arrives at Investment Committee memos with more time to pressure-test the thesis. Data maturity does not guarantee outcomes on its own, but it can improve decision velocity and reduce friction at critical moments.

Portfolio monitoring and value creation

Post-acquisition, the ability to aggregate and normalize portfolio company data determines how quickly an asset manager can identify underperformance and intervene. Manual quarterly reporting cycles mean problems surface three to four months after they start.

Automated data pipelines with quality controls surface issues in near-real-time. When a portfolio company’s gross margin compresses in a way that’s inconsistent with prior quarters, a firm with continuous monitoring flags it within days. Here, data maturity translates directly to MOIC: faster identification of value creation levers, earlier intervention on underperforming assets, more accurate exit timing based on actual data rather than lagged reports.

Investor reporting and LP confidence

LPs are asking for more granular, frequent, and standardized reporting. In private markets, ILPA templates represent the baseline, while institutional LPs increasingly want custom analytics layered on top. The ILPA Reporting Templates have expanded significantly, with enhanced fee reporting and diversity metrics reflecting a broader shift toward LP accountability expectations.

Companies that can produce accurate, consistent reports build LP trust in a way that shows up in fundraising conversations. Capital raising from existing LPs on favorable terms is, in itself, an IRR driver. Inconsistent or error-prone reporting, however, erodes the institutional confidence that makes those conversations go smoothly.

What asset managers at the frontier are doing differently

The pattern emerging among companies that have moved beyond manual, fragmented data operations comes down to two operational shifts. Neither of them require replacing the investment team’s existing tools overnight, but all of them change where the work happens.

1. Automating normalization and stitching at the ingestion layer

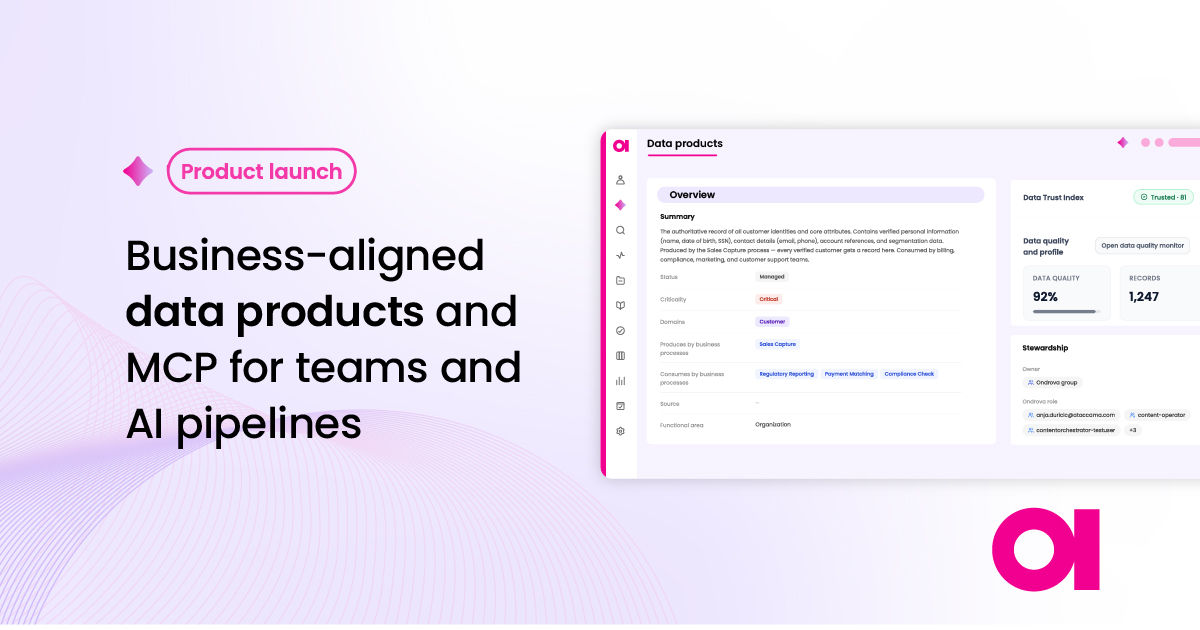

Rather than letting raw vendor data and portfolio company feeds flow into analyst spreadsheets, leading companies intercept data at the point of ingestion, apply automated quality rules, and normalize it against a common data model before it reaches the investment team. This means investment professionals start with clean, consistent data rather than spending time creating it.

Platforms such as Ataccama ONE’s are designed to operate at exactly this layer, by helping firms with data quality and observability capabilities. The platform monitors data as it flows through pipelines, flags anomalies before they reach downstream models, and routes exceptions to the right owners. When a portfolio company CFO sends a P&L with a different account structure than last quarter, the inconsistency is caught and resolved at ingestion rather than discovered halfway through a board presentation.

2. Validating vendor data before it impacts decisions

Instead of discovering data quality issues when a model produces unexpected results, businesses at the frontier apply automated validation rules at the point of vendor data ingestion. This means a data feed from Bloomberg or FactSet gets checked against expected schemas, value ranges, and internal reference data before it touches a valuation model or investor report.

This validation layer is precisely what distinguishes companies that have absorbed a vendor data quality incident from those that will in the future. According to the EY Global Private Equity Survey 2023, businesses with mature data and technology capabilities achieve more reliable decision-making, efficiency, and insight generation. The validation layer is a major part of how that accuracy gets built.

Measuring the impact

Isolating data maturity’s specific contribution to fund performance is difficult, but there are leading indicators that asset management firms can track. These indicators correlate strongly with lagging financial performance across fund vintages.

Proxy metrics worth monitoring include:

- Time from deal sourcing to Investment Committee memo

- Hours spent on data preparation versus analysis per deal

- Time to produce quarterly LP reports

- Number of manual reconciliation steps in the portfolio monitoring workflow

- Frequency of data issues identified late in the process rather than at ingestion

Better data operations free up investment professionals to do work that creates more value.

Ataccama’s data quality and observability capabilities provide the instrumentation to track these metrics automatically rather than through self-reported estimates, which means the measurement baseline itself stops being a manual exercise.

The specialization imperative

The companies that will generate top-quartile returns over the next decade are already treating data infrastructure as a core investment capability. Evidence for this accumulates through every stage of the investment lifecycle, from faster screening to earlier monitoring and cleaner reporting.

As AI-assisted deal screening, portfolio optimization models, and automated due diligence tools become standard in the asset class, the quality of upstream data becomes a constraint. Models trained on unreliable data produce unreliable outputs, and AI agents operating on fragmented, unnormalized data amplify errors.

The firms building the data foundation now are building the infrastructure on which the next generation of investment tools will run. It’s a compounding advantage that every asset manager can benefit from.

Want to see how Ataccama ONE helps asset management firms move from manual data reconciliation to an automated data trust layer?

Speak with a specialist to learn more.

Anja Duricic

Anja is our Product Marketing Manager for ONE AI at Ataccama, with over 5 years in data, including her time at GoodData. She holds an MA from the University of Amsterdam and is passionate about the human experience, learning from real-life companies, and helping them with real-life needs.